Why do two KKR funds, K-FIT with $1.54 billion in shareholder equity and K-ABF, both currently gating investor redemptions, need permission to co-invest?

private equity/credit + interval fund = alternative = 401(k) + retail + liquidity?

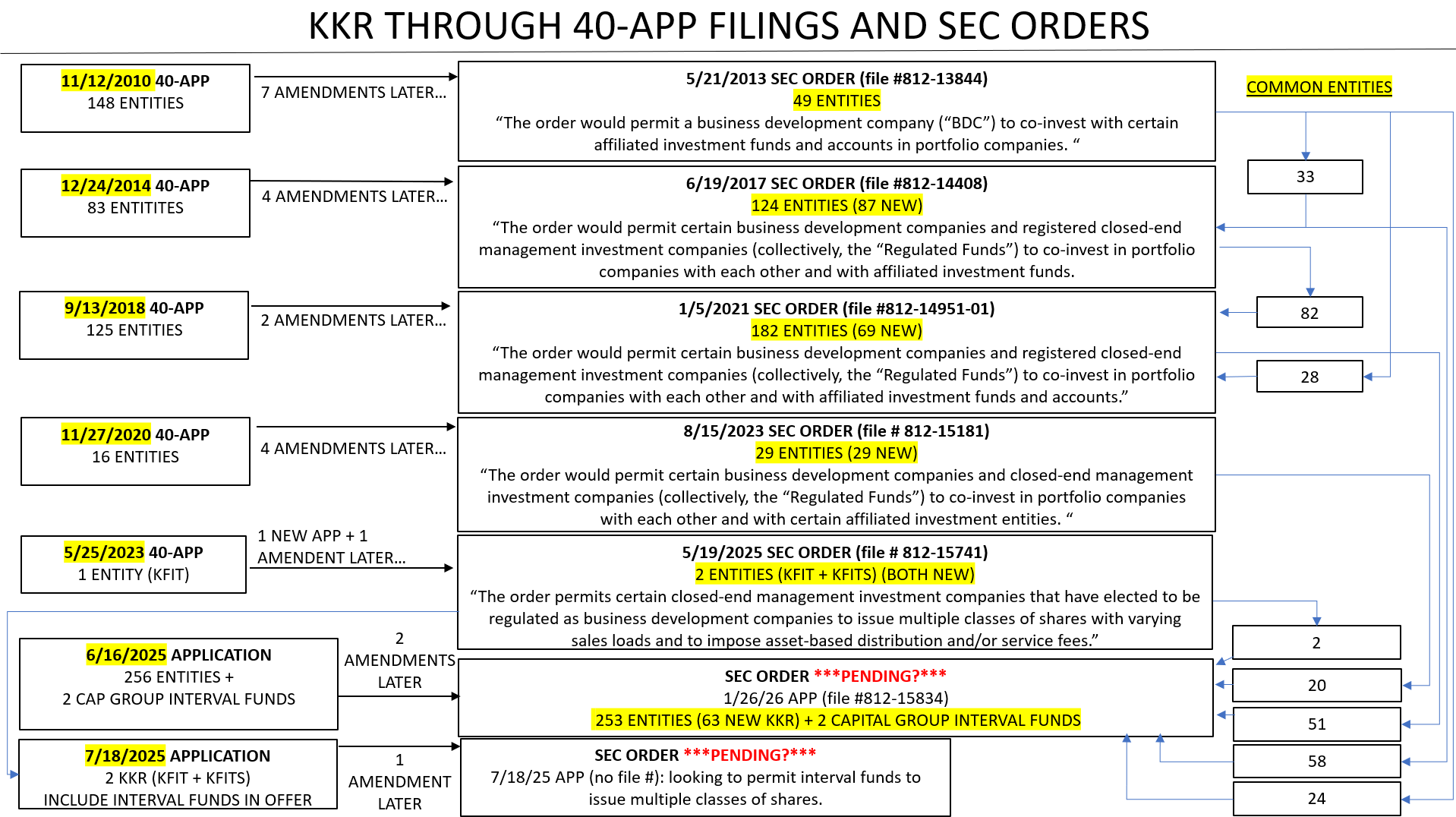

The chart traces some of KKR's 40-APP filings back to 2010. A 40-APP is a request to the SEC for permission to do something (sometimes things it would otherwise prohibit). The word co-invest appears in every SEC order approving these requests, except the 5/19/25 order, which addressed issuing multiple share classes. One of KKR's latest filings includes two Capital Group interval funds alongside its own entities.

Josh Brown on Compound and Friends Podcast: "Why aren't institutional investors pushing back harder on these marks? Like, if it's as obvious as you make it sound, which it may be, where is the pushback from the larger end investors?"

Answer: Larger investors are not pushing back. Capital Group is a multi-trillion-dollar asset manager, one of the best in the business, with analysts who have the kind of institutional access and credibility that makes their presence in this structure meaningful. Their presence here matters. A manager of that reputation doesn't partner carelessly, and having them in the structure presumably means someone has taken a hard look at KKR's books. The honest question is: who is taking a hard look at everyone else's?

Larger investors not pushing back may be the wrong question to ask. Larger investors have different motivations and time horizons than individual fund investors. Tracy Alloway, What Next TBD Podcast: "Why Everyone is Freaking Out about Private Credit": "the fundamental thing that is happening here, which is you have a lot of investors who are worried about getting out at the moment."

Dismissing private credit and equity concerns based on market size misses the point. The better question is whether allowing these assets to remain in their current form ties up capital that could go to more productive use.

These types of funds are but one example of how private credit/equity gets funded. Insurers are investors too, putting policyholder capital to work in these same structures. When excluding NDFI loans (which include loans to private equity funds, mortgage and business credit intermediaries, securitization vehicles, hedge funds, and similar entities) small banks have lent $1 trillion more in traditional loans and credit than large banks have over the last ten years. Meanwhile, large banks have lent over $800 billion more in NDFI loans over the same period. The risk didn't disappear. It redistributed, quietly, across a system with uneven oversight.

Jamie Dimon has said that well-designed bank regulations can free up capital and liquidity for productive use. The H8 data suggests that's not quite what happened.

Non-publicly traded assets can generate consistent income, which is invaluable for investors taking withdrawals from their portfolios. When stock and bond funds move in tandem, sequence of returns risk becomes very real for those taking withdrawals, and a portfolio that works well during accumulation can quietly fail the people who need it most. Perhaps having these assets in 401(k)'s and available to more investors is a net good thing for those who need the income, if it ultimately means investors pay less in fees and have a retirement account that actually works during the distribution phase. It would also put considerably more scrutiny on valuations. And that may be the thread running through all of this. The risk didn't originate outside the banking system, it migrated through it. Small banks absorbed the traditional lending, large banks moved into NDFI, insurers put policyholder capital to work alongside private equity, and the oversight scattered accordingly. If bank regulators already touch most of the funding chain, why not let them follow it all the way through?

On the markets side, perhaps the public markets will be just as good arbiters of risk as regulators are. Capital Group Capital Conversations Podcast with Mike Gitlin talking to New York equity analyst Cyana Chilton: "You look at the banks, and a lot of the bank CEO's, and I have the privilege to spend time with them, tell me "you know what, Cyana's great, and she helps us when we are thinking about our strategy."" When bank CEOs are asking Capital Group for strategic guidance, it is a safe bet they know what they are getting into when they decide to partner with KKR.

Whether this 40app means that KKR assets get added to the Capital Group interval funds remains unbeknownst to me. If that is the case, perhaps that means liquidity for KKR investors who want out.

What I could see happening here is that those who want out, are potentially getting a way out while those who don't want to sell are not being forced to. Banks and public markets together will work to keep asset prices honest.

The last KKR 40-APP amendment included two funds who gated investor redemptions, K-FIT and K-ABF. The newest amendment, filed April 27, 2026, adds Muskoka JV LLC. Hopefully not the same Muskoka that's flooding right now.

Jeff Gundlach 4/29/26 Closing Bell, negative on private credit + interval funds: "June 23rd is the Ides of June. It has something to do with the moon phase (it's not always the 15th of the month) and I think you're going to get humungous withdrawal requests from these interval funds."

Joe Weisenthal OddLots 4/30/26: "the value of people who can find information that has not turned into training data yet for a model, that data is going to get super valuable and maybe more valuable and more reason to just get out on the road and into stuff like that. "

Tracy Alloway: "I feel like the pendulum has swung from, for the past 20 years, if you were a smart person who could think in terms of numbers and code, you were probably very valued by society, and now the pendulum swings to those on-the-ground relationship-building social skills."

Any on the ground experts in cost of flood insurance in Muskoka Canada? Muskoka has over 1,600 lakes so I'm sure this has been priced in to some degree. Either you know someone with that data and/or are the person with that data.

api = associated person identity = $ value

*Capital Group KKR Core Plus+ and Capital Group KKR Multi-Sector+ are the two Capital Group interval funds named in the pending 812-15834 co-investment application.

{kind=link}

{kind=link}